Update, 4:40 PM: Here's hoping Dwight Cass finishes his analysis based on this, found in the prospectus, which Dealbreaker linked here:

No Golden Parachutes/CEO Compensation. We have no severance arrangements with any of our professionals. Accordingly, unlike in the case of many public companies, the departure of an executive officer or other senior managing director would not trigger any contractual obligation on our part to make any special payments to the departing professional. Moreover, following this offering Mr. Schwarzman will receive no compensation other than a $350,000 salary (and will own a significant portion of the carried interest earned from our carry funds).

Update, 5:25 PM: Here is a quick-link to their historical financial performance section. Scroll to page 98 for real estate activites. Summarized, as of 12/31/2006:

- Net Income from Fund Management Fees = $167.8 million (162% increase on 2005)

- Net Income from Investments = $735.0 million (151% increase)

- Assets under Management = $12.8 billion (21% increase)

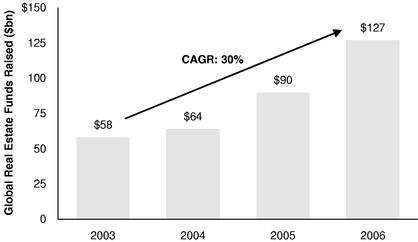

The real estate industry is also experiencing historically high levels of growth and liquidity driven by the strength of the U.S. economy, office employment growth, limited new construction and the availability of financing for acquiring real estate assets. Concurrently, replacement costs of real property assets have continued to escalate substantially. Since 2001, gross domestic product, or "GDP," growth has steadily improved, and GDP is currently predicted to grow at an average annual rate of approximately 3.1% from 2007 through 2009 as indicated by Haver Analytics, World Bank Indicators and Oxford Economic Forecasting. In addition, recent job growth statistics have indicated higher employment levels during 2005 and 2006, which generally produces greater demand for real estate assets. The strong investor demand for real estate assets is due to a number of factors, including persistent, reasonable levels of interest rates, the lack of alternative investments that provide the same levels of expected returns and the ability of lenders to repackage their loans into securitizations, thereby diversifying and limiting their risk. These factors have combined to significantly increase the capital committed to real estate funds from a variety of institutional investors, including institutional pension funds. As a result, the amount of global real estate funds raised has increased dramatically in the past four years, as indicated by the following chart:

Update, 6:00 PM: Real Estate Overview starts at the bottom of page 131. Here's a quicklink the closest page. Notables:

Update, 6:40 PM:

Real Estate happenings in the last 15 months:

That's about all I have the time and energy for right now. I'll be interested to see the multitude of other highlights as other bloggers dig through it as well...

- The prospectus highlights 11 acquistions of real estate companies, including the recent purchase of EOP. Excluding co-investors, Blackstone invested $7.2 billion in these acquisitions. Transaction values totaled $72.5 billion (90% leverage [again, including co-investments]).

Update, 6:40 PM:

Real Estate happenings in the last 15 months:

- Blackstone's Park Hill Group (now with 50 employees) expanded into raising equity for real estate funds in June 2006. Although the group was started in 2005.

- Their real estate operation opened an office in Mumbai in 2007.

That's about all I have the time and energy for right now. I'll be interested to see the multitude of other highlights as other bloggers dig through it as well...

No comments:

Post a Comment